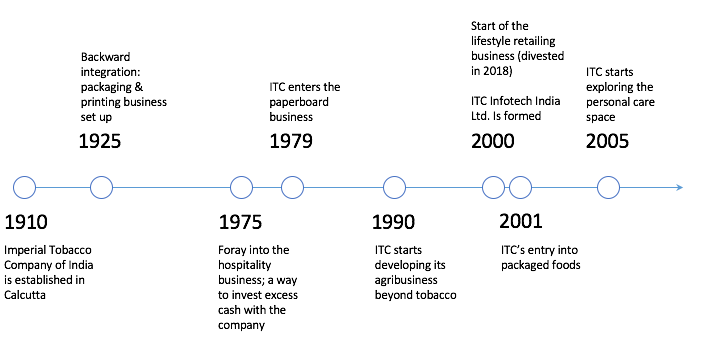

ITC’s roots go back a century. It was incorporated as Imperial Tobacco Company of India in 1910 and for the first 6 decades of its existence, it was devoted to growing and consolidating its cigarette and leaf tobacco business.

From cigarettes to hotels & what not

The winds changed direction in 1975. Since then, ITC’s growth trajectory has been punctuated by its foray into non-core businesses such as hotels and packaged foods. This diversification strategy underlines the company’s efforts to slowly but steadily steer its business away from tobacco. As a matter of fact, ITC aims to generate over ₹1 lakh crore in revenue by 2030, and it wants the bulk of the increase to come from its non-cigarette FMCG business.

Leaving cigarettes behind

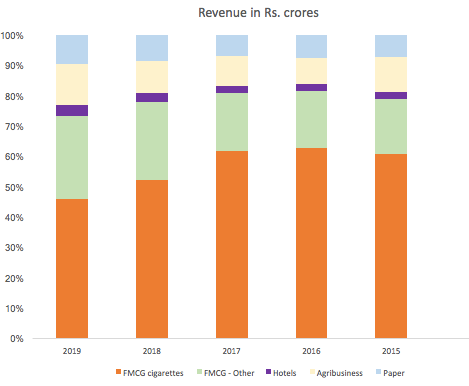

To be precise, the share of cigarettes in ITC’s top-line has been on a downward trajectory since 2016. Cigarettes’ fall from grace at ITC coincided with the decline of the legitimate cigarette industry in India plagued by high taxes. Even newer and supposedly “safer” products fail to get a sympathetic hearing — ITC is able to market Eon (e-vape) in only select states; 12 states have banned any sale of ENDS (Electronic Nicotine Delivery Systems).

Though cigarettes are on the verge of being dethroned, not all is lost for the mighty tobacco. Despite the somewhat erratic dwindling of Agribusiness, ITC is still the largest exporter of unmanufactured tobacco in India.

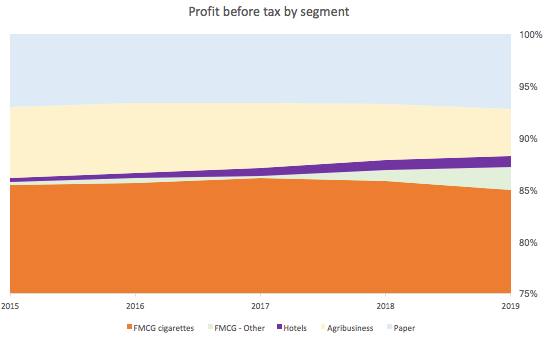

While these days ITC’s top brass rarely talks about tobacco, it’s the cigarette business that is actually keeping the wheels turning. The segment’s contribution to earnings* remains comparable to 2015 levels, although its share in revenue has fallen from ~60% in 2015 to 48% in 2019.

Milking the cash cow

Operations & heavy investments in non-cigarette businesses are financed by cash from the cigarette segment

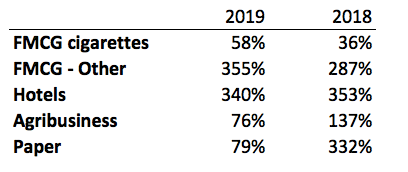

Although cigarettes still account for a whopping 85% of total earnings*, there are clear cut signs that ITC is itching to move away from its legacy business. CAPEX is greater than depreciation at the group level (a healthy 202%); but more than 80% of these investments are being made in other FMCG and hotels segment.

In recent years, ITC has been disinvesting in cigarettes — the asset investment ratio (CAPEX to Depreciation) for the segment is a lousy 58% in 2019. This exemplifies that the company is looking for growth outside of cigarettes — mostly in the other FMCG business segment.

Because the century-old company has negligible debt, the better part of earnings is used to shell out dividends which amounted to ₹6285 crores in 2019. This implies a payout ratio of close to 50% (higher than some of its tobacco-focussed peers).

Why shun the smoking sin for packaged food?

ITC’s main motivation to diversify its offerings probably result from its ambition to enhance its brand image and insulate itself from a cracky cigarette market subject to government’s whims. Steep rise in cigarette tax has led to the emergence of a robust illicit cigarette trade in India. In addition to causing huge tax losses to the exchequer, illegal cigarettes also punch a hole in ITC’s revenue numbers.

Given this backdrop, the packaged food industry seems promising. ITC already has a history of working closely with farmers (as part of its agribusiness segment) and it could leverage its knowledge of the Indian market to gain an edge over foreign brands.

In a nutshell…

ITC started changing direction by changing its name (ITC is no longer an acronym). Although it is not the first tobacco company to mix cigarettes with food, it the among the first ones to show remarkable resilience in taking its non-cigarette business forward. Rumour has it that the company’s next foray is in healthcare — who would’ve thought to mix tobacco with healthcare? We’re sure that Government of India doesn’t mind — it owns 30% of ITC.

*Earnings here refer to Profit Before Tax (PBT)